The UAE’s exit from OPEC is being read as an oil market headline. That is too narrow.

For the maritime professional, it may mark a structural shift in the Gulf’s energy geography. It marks the moment where terminal geometry becomes as important as production policy.

We are moving into a reality where Fujairah, Das Island, and the Strait of Hormuz no longer sit on the same risk map. The producer alignment has fractured, and the maritime industry is left to manage fragmented routing, volatile insurance premiums, and a redefined voyage operating envelope.

The effect will begin in the chartering, insurance offices, and refinery buying programs. But it will end with the Master executing a passage plan through a region where the traditional safety of a “unified bloc” has been replaced by a contested map of terminals and chokepoints.

The headline belongs to oil, the permanent consequence will be carried by ships.

For the current operational background on Hormuz transit risk, see DeepDraft’s earlier analysis on Hormuz routing shift, mine risk and the cost of transit in 2026.

Politics Does Not Move Ships. Cargo Does.

A political decision becomes material through its impact on fixtures, terminal calls, voyage orders, and navigational risk. Until then, it remains a headline.

The tanker market responds to nominated, lifted, financed, insured, and moved barrels. UAE policy freedom becomes a maritime factor only when exportable volumes increase, Asian refiners absorb them, and the security environment permits their movement.

Furthermore, maritime analysis departs from oil-market commentary at the point of operational execution:

- Oil analysts discuss barrels per day.

- Chartering desks find ships.

- Insurers price exposure.

- Terminals manage loading programs.

- Masters execute the voyage.

Tanker markets price the physical reality of cargoes, distance, delay, insurance, and the willingness of owners to accept risk.

The Gulf Producer Map Is Becoming Less Uniform

The UAE’s move alters the external perception of the Gulf producer bloc. Gulf crude strategy, historically treated as a coordinated structure led by Saudi Arabia, is now fracturing. Saudi Arabia maintains its central OPEC role, while the UAE pursues production flexibility and a more independent energy posture.

Crude flows rely on specific assumptions that are now shifting:

- Who cuts production?

- Who produces?

- Who prices aggressively?

- Who protects market share?

- Who supplies Asian refiners?

- Who maintains regional stability?

Tanker planning responds to these changes by monitoring different signals. Relevant indicators include fixtures, loading programmes, freight levels, terminal congestion, voyage amendments, and insurance instructions. Geopolitics translates into maritime operations the moment these signals deviate from established patterns.

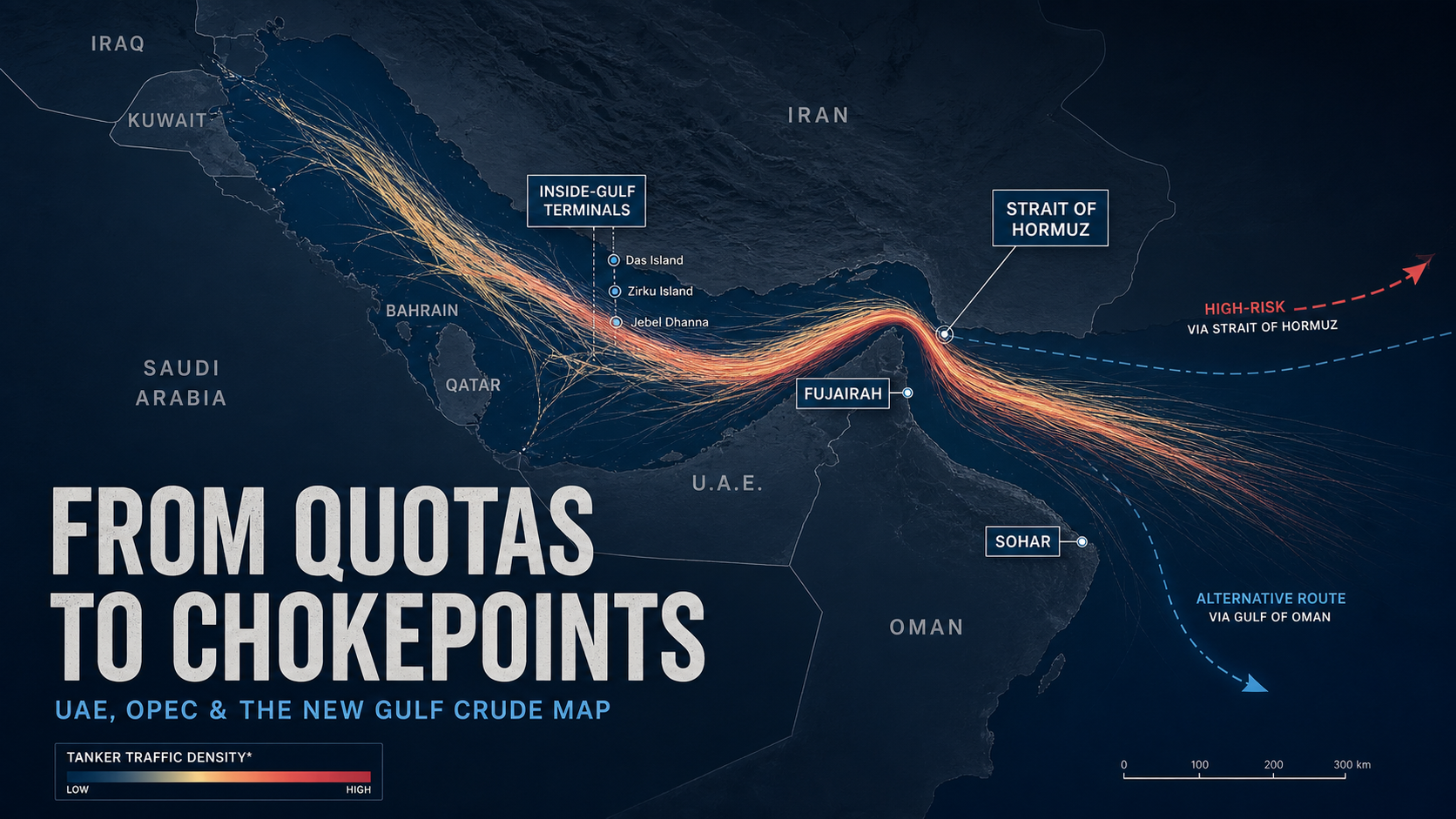

Credit: AFP / Bloomberg, using OSM, Copernicus and Global Maritime Traffic data.

The Geography Is the Real Maritime Story

The UAE is not a uniform export geography.

Fujairah, positioned outside the Strait of Hormuz, is strategically distinct from Abu Dhabi’s inside-Gulf export terminals. The Habshan-Fujairah pipeline has been pumping Murban crude since 2012 with a transmission capacity of 1.8 million barrels per day. ADNOC identifies both Fujairah and Jebel Dhanna as export terminals, yet these facilities occupy vastly different maritime risk geographies.

Inside the Gulf, the picture is constrained. ADNOC operations at Das Island and Zirku Island involve processing, storage, and export. In a Hormuz-risk scenario, these terminals remain exposed, unlike the Fujairah outlet. This split geography defines the maritime story. ADNOC has offered clients the option to load Das and Upper Zakum crude outside the Gulf to bypass Hormuz via ship-to-ship (STS) transfers off Fujairah or Sohar. The central question is no longer just production volume. Availability is dictated by location. Quotas have been replaced by chokepoints.

Fujairah, Khor Fakkan and Kalba Should Not Be Treated Alike

The UAE’s Gulf of Oman coastline provides a maritime advantage, but these locations are not interchangeable.

Fujairah is the established crude-export hub. It possesses the Habshan-Fujairah pipeline connection, significant oil storage, and high anchorage activity outside the Strait. Operationally, Fujairah serves as the primary bypass point for UAE crude.

Fujairah is not just an export terminal; it is a premier global bunkering hub. If crude exports surge alongside a fleet waiting out Hormuz disruptions, the anchorage will heavily congest. Ships calling for bunkers, crew changes, or provisions may face extended delays, tightening laycans and forcing Masters to recalculate reserves.

Khor Fakkan occupies a different risk profile. Historical crude STS and sanctions-risk advisories make the location sensitive rather than a confirmed clean alternative-loading point. Gard reported in 2015 that shipowners were targeted in attempts to export Iranian-origin crude through STS transfers at Khor Fakkan, often misdescribed as Iraqi origin. Steamship Mutual noted similar feeder-vessel activity between Iran and the UAE using falsified documentation. This history is relevant because STS operations involve commercial and sanctions sensitivity if cargo origin or documentation is unclear. Kalba occupies a third operational category. Geographically situated outside Hormuz, it has appeared in open-source reporting around emergency lighterage and refuge-type operations, including the 2020 MT New Diamond salvage context. That is operationally different from being a permanent, pipeline-fed crude export terminal.

Oman Becomes Part of the Workaround

Oman provides essential geographic leverage. ADNOC bypass arrangements involving STS transfers off Sohar elevate the port into a possible pressure-release valve for inside-Gulf barrels. It enables cargo to reach buyers while reducing Hormuz exposure for the receiving tanker.

This coastline establishes a practical interface that activates as inside-Gulf terminals face increased insurance premiums or operational friction. Tanker operators must increasingly prioritize this region during fixture planning, STS due diligence, and security assessments.

For the bridge team, an outside-Gulf STS order introduces a vastly different operational profile compared to a conventional terminal call. The envelope expands immediately to require alternate voyage planning, POAC arrangements, fendering logistics, rigid weather limits, and elevated sanctions checks. A vessel ordered to load via STS off the Omani coast operates in a much more exposed environment than one alongside a berth at Jebel Dhanna or Das Island. If there is a mechanical failure, a medical emergency, or a sudden weather deterioration during an offshore STS, the vessel’s options for a safe haven are severely limited compared to the infrastructure available deep inside the Gulf.

Where the Bridge Actually Enters

The bridge enters as producer policy and regional rivalry convert into operational instructions. While war defines today’s risk, the long-term maritime story is the divergence of the UAE from the Saudi-led framework.

That operating envelope is already complicated by electronic-navigation risk, including the GNSS interference and spoofing environment previously examined by DeepDraft in the Strait of Hormuz.

Condition: With War / Tactical Friction

- Immediate reliance on “War Risk” clauses and additional reporting.

- Direct naval coordination and exclusion-zone guidance.

- Physical security assessments for every loading window inside the Gulf.

Condition: Without War / Structural Reality

- Segmented Routing: The UAE’s outside-Hormuz infrastructure (Fujairah) creates a permanent operational separation from “Inside-Gulf” neighbors.

- Infrastructure Segregation: Managing the physical difference between the Habshan-Fujairah “Bypass” and conventional terminals requires distinct bridge and deck preparations.

- Conflicting Directives: Competing production targets between neighbors result in tightened ETAs and sensitive laycans as producers vie for refinery slots.

- Insurance Complexity: Even in peace, vessels calling at different Gulf ports may face varied premiums based on individual state risk profiles rather than a uniform bloc rate.

The bridge becomes involved through the operational consequences of these opaque shifts.

Command Under Ambiguity

The Master manages a crowded operating environment including machinery reliability, crew fatigue, and digital communication overload. Macro events like the UAE-OPEC split become relevant to the bridge as they add ambiguity to these existing pressures.

While war defines the immediate risk, the long-term “Opaque” reality is a shift from a predictable regional bloc to a competitive, fragmented maritime landscape.

Operational Indicators for Masters and Operators

- Tactical: Increased reliance on war-risk circulars, naval coordination, and security-driven routing restrictions.

- Structural : UAE-linked loading programme changes, additional nominations from Fujairah, and VLCC fixtures tied to UAE export growth.

- Bridge Pressure: Compressed decision time within deteriorating security pictures and charterer pressure to maintain schedules.

- STS Weight: Instructions for transfers outside the Gulf require intense risk assessment, fendering arrangements, and strict weather-window discipline.

Crucially, as legitimate UAE cargoes shift to STS operations off Fujairah or Sohar, they will increasingly share anchorage space with the “dark fleet” conducting sanctions-evading transfers. For the Master and the chartering desk, this drastically elevates the burden of counterparty due diligence. The bridge isn’t just worried about fenders and weather windows; they must rigorously verify the identity, AIS history, and ownership of the lightering vessel approaching them to ensure they aren’t inadvertently handling tainted cargo.

Credit: Image: James Fisher Fendercare.

This connects directly with DeepDraft’s earlier analysis on the Master’s role in OFAC compliance, where sanctions exposure becomes an operational problem rather than only a legal one.

Command must recognize when oil politics alters the operating envelope. Operators must distinguish between Fujairah crude movements and any Khor Fakkan-area STS activity where sanctions due diligence becomes critical.

For the bridge, the story begins when those decisions become operational instructions.

The DeepDraft View

The UAE’s departure from OPEC is a maritime strategy event because it may reshape how Gulf crude is produced, priced, lifted, insured and routed.

The core maritime question extends beyond production volumes. It is about the physical location of supply: whether barrels load inside the Gulf, move through Fujairah, become available outside Hormuz through STS transfers off the Gulf of Oman, or remain tied to terminals exposed to the Strait.

For tanker operators, the critical signals are the fixture list, the terminal programme, war-risk instructions, STS arrangements and the voyage order. For the Master, the headline matters when it becomes a specific operating condition on board the vessel.

That is the maritime point.

The headline belongs to oil. The consequence, if it develops, will be carried by ships.

Media Section

Sources

Sources

Reuters – UAE exit from OPEC/OPEC+ and OPEC+ output-policy context.

Reuters – ADNOC option for Das and Upper Zakum crude to load outside the Gulf, including possible STS off Fujairah or Sohar.

International Energy Agency – Strait of Hormuz crude-flow volumes, Asia exposure and alternative-route context.

Port of Fujairah – Habshan-Fujairah pipeline, Murban crude movement and 1.8 million barrels per day transmission capacity.

ADNOC Offshore – Das Island and Zirku Island crude processing, storage and export operations.

ADNOC Logistics & Services – Abu Dhabi petroleum ports including Jebel Dhanna, Das Island, Zirku Island and Mubarraz.

Gard – STS sanctions-risk advisory involving Iranian-origin crude and Khor Fakkan.

Steamship Mutual – STS transfer risk, feeder-vessel activity and falsified cargo-origin documentation around Khor Fakkan.

Merchant Marine General Directorate – MT New Diamond investigation report, including Kalba Anchorage / STS discharge context.

Reuters – Fujairah crude-loading disruption and Fujairah’s role as a Gulf of Oman crude and bunkering hub.

Leave a Reply